As we’re writing this, there are officially over 150,000 COVID-19 cases in Mexico, where BFA Global and MetLife Foundation have launched FinnSalud, a 3.5-year program focused on financial health, helping cooperatives and their members withstand the impacts of the pandemic. During this crisis, financial service providers (FSPs) focusing on low- to moderate-income populations are particularly vulnerable due to increasing liquidity constraints, and have critical roles to play to help clients weather the storm.

An initial step that complements broader agile scenario planning, portfolio stress testing is a risk management best practice that can help institutions understand the leading indicators and potential outcomes for the institution. It simulates how a financial institution’s portfolio and financials would perform against a set of possible scenarios to identify and gauge risks, giving management insights to understand and mitigate vulnerabilities. The COVID-19 pandemic creates both an urgency and a context for stress testing.

The COVID-19 pandemic creates both an urgency and a context for stress testing.

In the wake of the pandemic, there are key risks related to portfolios, operations, and levels of capital, so we have developed a Guide of Operational Suggestions and a Stress Testing Model to help cooperatives better prepare.

Setting the End-Client Context

Before jumping into the financial modeling side of the stress testing process, we built an informed view of the potential drivers and changes in behavior of FSP end clients. Concurrent to the stress testing process, BFA Global has researched the impact of COVID-19 on financial health in eight markets, including Mexico. This research indicates that incomes are already impacted and expenses have increased, putting significant pressure on cash flow, among many other new challenges.

Among the eight countries studied, Mexican small businesses and entrepreneurs have access to an extremely limited cash and asset cushion to draw from, and face the highest pressure to potentially close their enterprises if the shutdown continues for an extended period of time. Insights from this research and interactions with our cooperative partners revealed multiple factors that we have had to incorporate into our thinking and stress testing:

- Cash flow pressure will reduce members’ ability and willingness to dedicate limited resources toward loan repayments.

- Restrictions on movement will make it more difficult to interact with existing clients and will reduce their ability to visit branches.

- Reduced income will force many people to draw on savings to meet immediate needs.

- FSPs may need to close branches and limit or cease field operations by loan officers and/or agents.

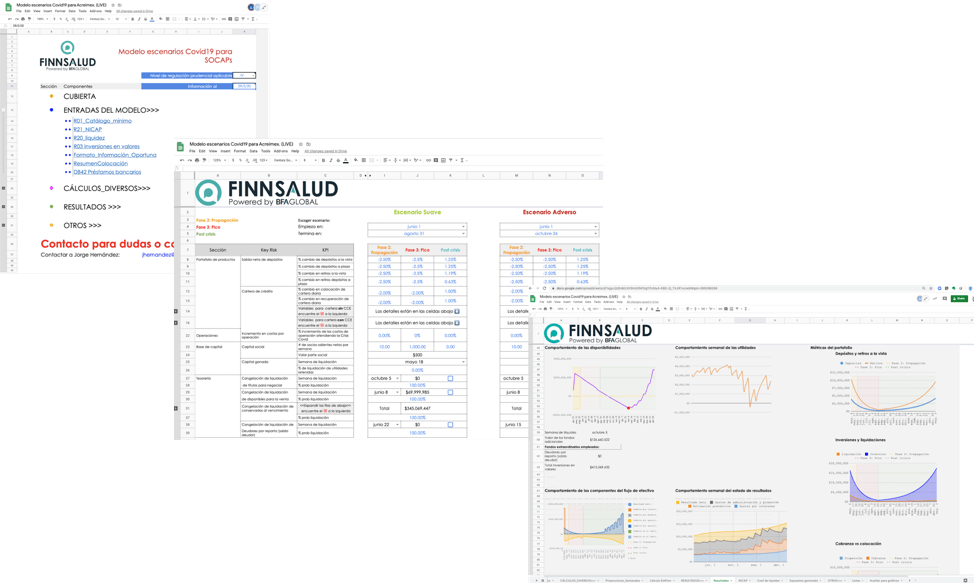

Stress Testing Model for Cooperatives

The open-source stress testing model considers three phases of the coronavirus crisis:

Propagation: The adverse effects on economic activity begin to be felt.

Peak: A large part of the population is confined to their homes and few economic activities are carried out.

Post-crisis: The economy begins to open to the new normal.

While developed within the Mexican cooperative context, this tool and process can be useful to a wider range of financial institutions grappling with the COVID-19 crisis globally. The model calculates key performance indicators (KPIs) for each risk category with different levels of intensity.

Primary Components of the Model

Inputs

Primary data fed into the model includes financial statements, past inflows and outflows – such as deposits and withdrawals from savings and current accounts and term deposits – average loan disbursements and payments, and effects of some government measures. Some of the regulatory reports that the cooperatives are required to send to the Comisión Nacional Bancaria y de Valores (National Banking and Securities Commission) – including minimum catalog, investments in securities, bank loans, liquidity ratio and capitalization requirements – are also used as inputs, as well as the timely information on COVID-19’s impact on a portfolio.

Calibration

After loading these inputs into the model, FSPs are given options to set the timeframes for each phase of the crisis, and calibrate the input variables for the two scenarios under four dimensions:

- Institutional portfolio (loans, savings, term deposits)

- Change in operations due to COVID-19

- Capital

- Liquidity management of treasury assets

Outputs

From the initial situation, the model calculates, on a weekly basis, the balance sheet, income statement, available cash balance and regulatory indicators of the liquidity ratio and the level of capitalization according to the conditions that the cooperative expects to face.

Deploying the Stress Testing Model with FinnSalud Cooperative Partners

BFA Global has been working with two Mexican savings and credit cooperatives as part of the FinnSalud program. These organizations serve a client base that is largely low-to middle-income and offer a suite of products that includes savings, term deposits, loans, payments, insurance and more.

We began the stress testing process with FinnSalud partners in late April as Mexico entered Phase 3 of the coronavirus pandemic, with government measures enacted to promote social distancing, further reduce movement, and restrict non-essential economic activity to lower the risk of overwhelming the country’s health system.

In the Mexican cooperative context, we considered two COVID-19 impact situations: a soft scenario and a worst-case scenario. Furthermore, our stress testing with cooperative partners focused on a few key variables:

- non-performing loans as a percentage of overall portfolio,

- growth (or reduction) in client base and issuance of new loans, and

- member savings, as measured by average weekly amount of withdrawals per client, and the percentage of the client base making a withdrawal each week.

These variables largely drive bottom line impact and, more importantly, cooperatives’ cash flow and liquidity levels.

While the stress test outputs and exact results will be different for each institution, we found a few insights that could help the broader financial inclusion and financial health sectors and other FSPs as they embark on a similar journey.

Through multiple scenarios, we saw the percentage of non-performing loans grow to over 50 percent within a month of projected lockdowns. This massively reduces interest income for the FSP. An initiative deployed by the Mexican regulator is to allow FSPs to continue recognizing interest revenue for a number of months during the crisis, during which time, certain customers are given a moratorium on actual payments over the same period. Based on our observations thus far, this benefit would accrue to one out of five debtors.

Across multiple scenarios, deposits are expected to decrease while withdrawals increase consistently over the first few months of the lockdown. While it may seem counterintuitive initially, FSPs may be best served in the medium and longer terms to make it easier for clients to access savings to a certain point. As an alternative to withdrawing funds from savings or current accounts, cooperatives might, for example, enable access to funds via loans with special interest rate conditions or loan terms.

As with most parts of the global economy, cooperatives have had to shift part of their teams to remote work and, for those who are able to, shift interactions with clients to digital and remote channels as well. This brings an urgent need to quickly identify and deploy digital tools to support the internal workforce in executing components of their jobs remotely. And as movement restrictions more or less halt all new client sign ups, FSPs will need to explore shifting field officers over to a remote customer care function temporarily.

We don’t know what the future holds, but we do know that building robust financial projections is essential for FSPs. At BFA Global, we hope that the stress testing tool and suggested operational guidelines will assist financial services partners to be as well-prepared as possible. The 8 million low and moderate-income Mexicans who rely on savings and credit cooperatives for services will greatly value it.

All opinions are BFA Global’s. Our funders are not responsible for the information presented herein, nor for its use.

Explore More