Abstract

The lack of a behavioral isomorphism between theoretically equivalent auction institutions is a robust finding in experimental economics. Using a near-continuous time environment and graphically adjustable bid functions, we are able to provide subjects with extensive feedback in multiple auction formats. We find that (1) First Price and Dutch Clock auctions are behaviorally isomorphic and (2) Second Price and English Clock auctions are behaviorally isomorphic. We further replicate the established result (1) that prices in Dutch Clock auctions exceed those of English Clock auctions and (2) that prices in First Price auctions exceed those of Second Price auctions. The latter pattern is often attributed to risk aversion which changes the equilibrium bidding strategy for First Price and Dutch Clock auctions. Because we observe each participant’s bid function directly, we find evidence suggesting a different explanation, namely that bidders are best responding to the distribution of observed prices.

Similar content being viewed by others

Notes

There have been some previous experiments that solicited bid functions. For example, Kirchkamp et al. (2009) asked subjects provide bids for six possible value realizations and then linearly imputed bids for other values.

Davis and Korenok (2009) show that such near-continuous time experiments enable subjects to gain considerable experience which leads to behavioral outcomes that are consistent with competitive predictions even when more standard experimental approaches (with less feedback and experience) do not.

Perhaps the most common theoretical explanation for the observed price differences between first price and second price sealed bid auctions and between Dutch Clock and English clock auctions is that bidders are risk averse (see Cox et al. 1982). Other explanations for over bidding relative to the risk neutral equilibrium predictions for first price auctions include a flat maximum critique (Harrison 1989), winner regret (Engelbrecht-Wiggans 1989) convex probability weighting (Goeree et al. 2002), learning models (Ockenfels and Selten 2005; Neugebauer and Selten 2006), and loser regret (Englerbrecht-Wiggans and Katok 2008).

For a recent review of Dutch Clock auction experiments see Adam et al. (2017).

The instructions are provided in an online appendix on the journal’s website.

Twelve auctions were conducted in the typical manner so that on average each subject would win four auctions.

Using the difference between the average earnings of males and females within a group of N = 4 bidders, a sign test fails to reject the null hypothesis that males and females earned the same amount in treatments involving the Second Price and English auctions (p = 1.000). Males, however, earn more in the treatments involving First Price and Dutch auctions (p = 0.012).

For the Dutch auction this expectation assumes risk neutral bidders following the equilibrium bid function.

This pattern would be surprising if the similarity in prices between theoretically equivalent formats was due to the near-continuous time nature of the environment making the clock less salient.

When using all of the near-continuous auction data the p values are 0.246 and 0.313, respectively, for the Wilcoxon signed rank tests.

When using all of the near-continuous data the p values are less than 0.001, for each of the pairwise Wilcoxon rank sum tests.

Our use of the last 50 periods here and elsewhere in the paper is arbitrary. The qualitative results are robust to other durations.

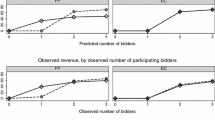

Averages are taken for each value from 0 to 10 in 0.1 increments.

Specifically, we assume that utility is represented by U(x) = xr.

Best responses to observed distribution of prices yields discontinuous best response curves because of the discrete nature of realized prices.

While Fig. 4 is suggestive, this explanation was developed ex-post. Because our experiment was not designed to test this idea, we leave doing so to future research.

The difference between a subject’s bid in the Dutch and First Price auction was regressed on a constant term. Similarly, the difference between a subject’s bid in the English and Second Price auction was regressed on a constant term. Figure 6 plots the p values associated with these constants.

The software forced the subjects to place a bid of zero when the value was 0.

Care should be taken when considering regression results as the tests are not independent across values since they are based on the same bid function. This is why the p values are continuous.

References

Adam, M., Eidels, A., Lux, E., & Teubner, T. (2017). Bidding behavior in Dutch auctions: Insights from a structured literature review. International Journal of Electronic Commerce,21(3), 363–397.

Aloysius, J., Deck, C., & Farmer, A. (2012). Price bundling in competitive markets. Journal of Revenue and Pricing Management,11(6), 661–672.

Coppinger, V., Smith, V., & Titus, J. (1980). Incentives and behavior in English, Dutch, and sealed-bid auctions. Economic Inquiry,18(1), 1–22.

Cox, J., Roberson, B., & Smith, V. (1982). Theory and behavior of single object auctions. In V. L. Smith (Ed.), Research in experimental economics. Greenwich: JAI Press.

Cox, J. C., Smith, V., & Walker, J. (1983). A test that discriminates between two models of the Dutch-first auction non-isomorphism. Journal of Economic Behavior & Organization,4(2), 205–219.

Cox, J., Smith, V., & Walker, J. (1988). Theory and individual behavior of first-price auctions. Journal of Risk and Uncertainty,1, 61–99.

Davis, D., & Korenok, O. (2009). Posted offer markets in near-continuous time: An experimental investigation. Economic Inquiry,47(3), 449–466.

Deck, C., Lee, J., Reyes, J., & Rosen, C. (2013). A failed attempt to explain within subject variation in risk taking behavior using domain specific risk attitudes. Journal of Economic Behavior & Organization,87, 1–24.

Deck, C., & Wilson, B. (2002). The effectiveness of low price matching in mitigating the competitive pressure of low friction electronic markets. Electronic Commerce Research,2, 385–398.

Deck, C., & Wilson, B. (2006). Tracking customer search to price discriminate. Economic Inquiry,44(2), 280–295.

Deck, C., & Wilson, B. (2008). Experimental gasoline markets. Journal of Economic Behavior & Organization,67(1), 134–149.

Duong, Q., & Lahia, S. (2011). Discrete choice models of bidder behavior in sponsored search. In N. Chen, E. Elkind, & E. Koutsoupias (Eds.), Internet and network economics. WINE 2011. Lecture notes in computer science (Vol. 7090). Berlin, Heidelberg: Springer.

Edelman, B., Ostrovsky, M., & Schwarz, M. (2007). Internet advertising and the generalized second price auction: Selling billions of dollars worth of keywords. American Economic Review,97(1), 242–259.

Engelbrecht-Wiggans, R. (1989). The effect of regret on optimal bidding in auctions. Management Science,35(6), 685–692.

Goeree, J., Holt, C., & Palfrey, T. (2002). Quantal response equilibrium and overbidding in private-value auctions. Journal of Economic Theory,104(1), 247–272.

Güth, W., Ivanova-Stenzel, R., Königstein, M., & Strobel, M. (2003). Learning to bid: An experimental study of bid functions adjustments in auctions and fair division games. The Economic Journal,113(487), 477–494.

Harrison, G. (1989). Theory and misbehavior of first-price auctions. The American Economic Review,79(4), 749–762.

Harstad, R. (2000). Dominant strategy adoption and bidders’ experience with pricing rules. Experimental Economics,3(3), 261–280.

Holt, C., & Laury, S. (2002). Risk aversion and incentive effects. The American Economic Review,92(5), 1644–1655.

Kagel, J. (1995). Auctions: A survey of experimental research. In J. Kagel & A. Roth (Eds.), The handbook of experimental economics (pp. 501–585). Princeton, NJ: Princeton University Press.

Kirchkamp, O., Poen, E., & Reiss, J. (2009). Outside options: Another reason to choose the first-price auction. European Economic Review, 53(2), 153–169.

Lucking-Reiley, D. (1999). Using field experiments to test equivalence between auction formats: Magic on the internet. American Economic Review,89(5), 1063–1080.

Neugebauer, T., & Selten, R. (2006). Individual behavior of first-price auctions: The importance of information feedback in computerized experimental markets. Games and Economic Behavior,54(1), 183–204.

Ockenfels, A., & Selten, R. (2005). Impulse balance equilibrium and feedback in first price auctions. Games and Economic Behavior,51(1), 155–170.

Ostrovsky, M., & Schwarz, M. (2016). Reserve prices in internet advertising auctions: A field experiment. Working paper, Stanford University.

Smith, K., & Dickhaut, J. (2005). Economics and emotion: Institutions matter. Games and Economic Behavior,52, 316–335.

Turocy, T., Watson, E., & Battalio, R. (2007). Framing the first-price auction. Experimental Economics, 10(1), 37–51.

Weber, E. U., Blais, A., & Betz, N. E. (2002). A domain-specific risk-attitude scale: Measuring risk perceptions and risk behaviors. Journal of Behavioral Decision Making,15, 263–290.

Acknowledgements

We thank Jeff Kirchner for brilliantly programming the software, Megan Luetje for recruiting the participants, Chapman University for funding the participant payments, and feedback from James Cox, participants at the Economic Science Association meetings, the editor and two anonymous reviewers.

Author information

Authors and Affiliations

Corresponding author

Additional information

Publisher's Note

Springer Nature remains neutral with regard to jurisdictional claims in published maps and institutional affiliations.

Electronic supplementary material

Below is the link to the electronic supplementary material.

Rights and permissions

About this article

Cite this article

Deck, C., Wilson, B.J. Auctions in near-continuous time. Exp Econ 23, 110–126 (2020). https://doi.org/10.1007/s10683-019-09603-4

Received:

Revised:

Accepted:

Published:

Issue Date:

DOI: https://doi.org/10.1007/s10683-019-09603-4